The details of the Finance Bill 2021 have been published by the government.

The Bill outlines the key measures set to be brought into legislation, including many measures announced in the recent 2021 Budget.

In his Budget speech, Chancellor Rishi Sunak announced an extension of the stamp duty holiday in England; a super-deduction capital allowance; extensions of the Coronavirus Job Retention Scheme (CJRS) and the Self-employment Income Support Scheme (SEISS); and an extension of the VAT cut for the tourism and hospitality sectors.

The Bill will make sure the measures announced in the Budget take effect from 6 April 2021. It also legislates for tax changes that were previously consulted on and subsequently confirmed at the Budget.

The government is to extend business rates relief with a £1.5 billion fund targeted at those businesses unable to benefit from the current COVID-19 support.

Retail, hospitality and leisure businesses have not been paying any rates during the pandemic, as part of a 15 month-long relief which runs to the end of June this year.

However, many businesses ineligible for reliefs have been appealing for discounts on their rates bills, arguing the pandemic represented a ‘material change of circumstance’ (MCC).

The government says that market-wide economic changes to property values, such as from COVID-19, can only be properly considered at general rates revaluations, and will therefore be legislating to rule out COVID-19 related MCC appeals.

Instead, the government will provide a £1.5 billion pot across the country that will be distributed according to which sectors have suffered most economically, rather than on the basis of falls in property values. It says this will ensure the support is provided to businesses in England in the fastest and fairest way possible.

Chancellor of the Exchequer Rishi Sunak said:

‘Our priority throughout this crisis has been to protect jobs and livelihoods. Providing this extra support will get cash to businesses who need it most, quickly and fairly.

‘By providing more targeted support than the business rates appeals system, our approach will help protect and support jobs in businesses across the country, providing a further boost as we reopen the economy, emerge from this crisis, and build back better.’

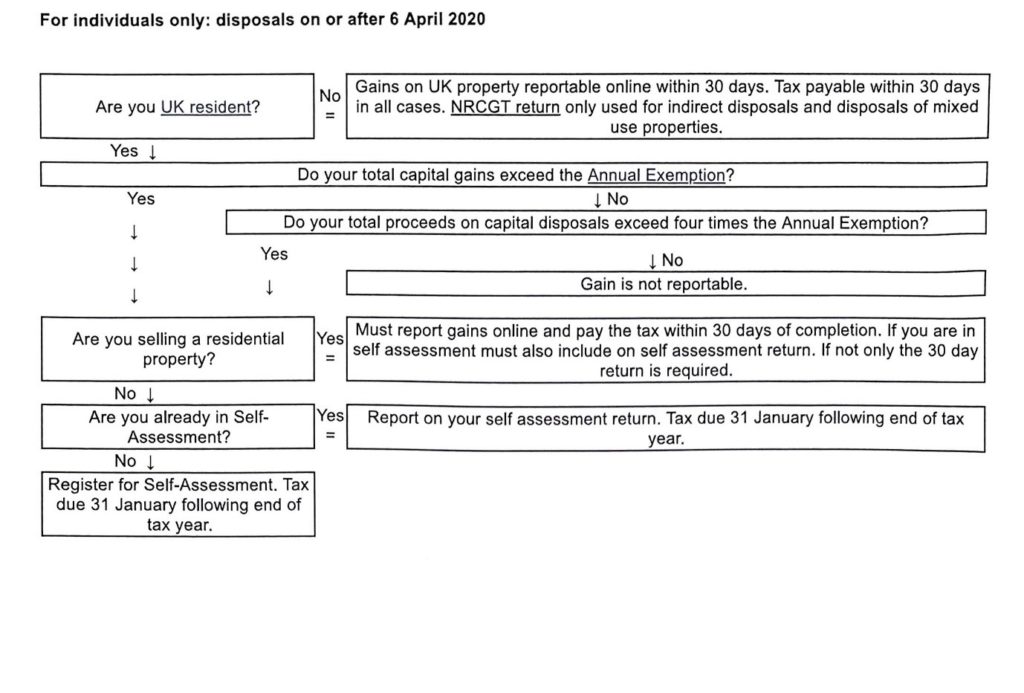

Selling a Residential Property and reporting the Sale to HMRC

In the Budget the Chancellor extended the period for Zero stamp duty on property purchases up to £500,000 until the 30th June 2021. After this date the zero threshold will reduce to £250,000 up to the 30th September 2021 and then drop down to £125,000.

This is great news for buyers and a further boost to the housing market.

Please remember that if you are buying a second property then the additional stamp duty still applies at a 3% surcharge.

Property bought in a company however will benefit from the new rates up to the 30th June 2021 provided the property is under the £500,000 limit.

Ask us for advice on this aspect if you are looking to buy a residential property.

What if you are a seller?

As a seller this should increase your chances of selling your property but beware if the property is not your main residence and you have potential capital gains tax to pay you must report the sale within 30 days to HMRC.

This new legislation came in for disposals after 6th April 2020.

When do I have Capital Gains Tax To Pay?

If the property is your main home, then you will not have to pay capital gains tax as it qualifies for Principle Property Relief.

If however you own another residential property perhaps you have bought a holiday home that just the family uses, you have bought a property for your children to live in whilst at university or you have residential property that you let out, then the new legislation may apply to you.

Capital Gains Tax is calculated based on the price you sell the property for after allowing for the price you paid for the property less other deductible costs.

Will It Apply to Me?

The flow chart below is a simple guide as to whether you will have to report the sale to HMRC.

What to Do to report the Gain

Step One

Work out if you have any capital gains tax to pay on the property. To do this you will need the following information:

calculations for each capital gain or loss you report

details of how much you bought and sold the asset for

the dates when you took ownership and disposed of the asset

any other relevant details, such as the costs of disposing of the asset and any tax reliefs you’re entitled to

If you have a gain then move on to :

Step Two

Create a Capital gains Tax Gateway account with HMRC if you do not already have one

This must be done within 30 days of the property disposal date.

Step Four

HMRC will send you a letter advising you what you owe and giving you a reference number and details of how to pay

Do I have to do anything else?

Yes, if you complete a self-assessment tax return the gain details should also be recorded on to this return as part of your normal self-assessment completion.

Don’t wait until the deadlines for your self-assessment return as you may then face interest on the capital gains tax due.

This is a complicated area of tax law and if you need any advice on this we can assist and complete the calculations and the returns on your behalf.

We can provide a quote for this work to be done for you – Obtain Quote Now

Businesses that took out government-backed Bounce Back loans to get through the coronavirus (COVID-19) pandemic will now have greater flexibility to repay their loans, the government has announced.

The Pay as You Grow repayment flexibilities now include the option to delay all repayments for a further six months. This means businesses can choose to make no payments on their loans until 18 months after they originally took them out.

Pay as You Grow will also enable borrowers to extend the length of their loans from six to ten years, which reduces monthly repayments by almost half.

They can also make interest-only payments for six months to tailor their repayment schedule to suit their individual circumstances.

The Pay as You Grow options will be available to more than 1.4 million businesses which took out a total of nearly £45 billion through the Bounce Back Loan Scheme (BBLS).

The Chancellor of the Exchequer, Rishi Sunak, said:

‘Businesses are continuing to feel the impact of extended disruption from COVID-19, and we’re determined to give them the backing and confidence they need to get through the pandemic.

‘That’s why we’re giving Bounce Back loan borrowers breathing space to get back on their feet, through greater flexibility and time to repay their loans on their terms.’

HMRC has announced that businesses that deferred VAT payments last year can now join the new online VAT Deferral New Payment Scheme to pay it in smaller monthly instalments.

To take advantage of the new payment scheme businesses will need to have deferred VAT payments between March and June 2020, under the VAT Payment Deferral Scheme. They will now be given the option to pay their deferred VAT in equal consecutive monthly instalments from March 2021.

Businesses will need to opt-in to the VAT Deferral New Payment Scheme. They can do this via the online service that opened on 23 February and closes on 21 June 2021.

Jesse Norman, Financial Secretary to the Treasury, said:

‘The Government has provided a package of support worth over £280bn during the pandemic to help protect millions of jobs and businesses.

‘This now includes the VAT Deferral New Payment Scheme, which will help provide businesses with the breathing space they may need to manage their cashflows in the weeks and months ahead.’

What to Do to report the Gain

What to Do to report the Gain